portability estate tax return

Thanks to ATRA it no longer has to be renewed to remain in effect. Portability is a planning tool available only to married couples.

Historical Estate Tax Exemption Amounts And Tax Rates 2022

If you dont file the 706 at the first death you cannot elect to port over this remaining amount.

. The Impact of the Portability of the Federal Estate Tax Exclusion Example 1. The term election here means a decision made by checking a box on a tax return. So this is a discussion you can have with the family to make sure they understand the cost and the potential benefits of portability and they can make the right decision of whether or not to make.

Opting Out The estate of a decedent with a surviving spouse which files Form. DSUEA on IRS Form 706 Estate Tax Return Part 6 A. Portability should remain a permanent part of federal estate tax law going forward unless Congress takes step to repeal this provision.

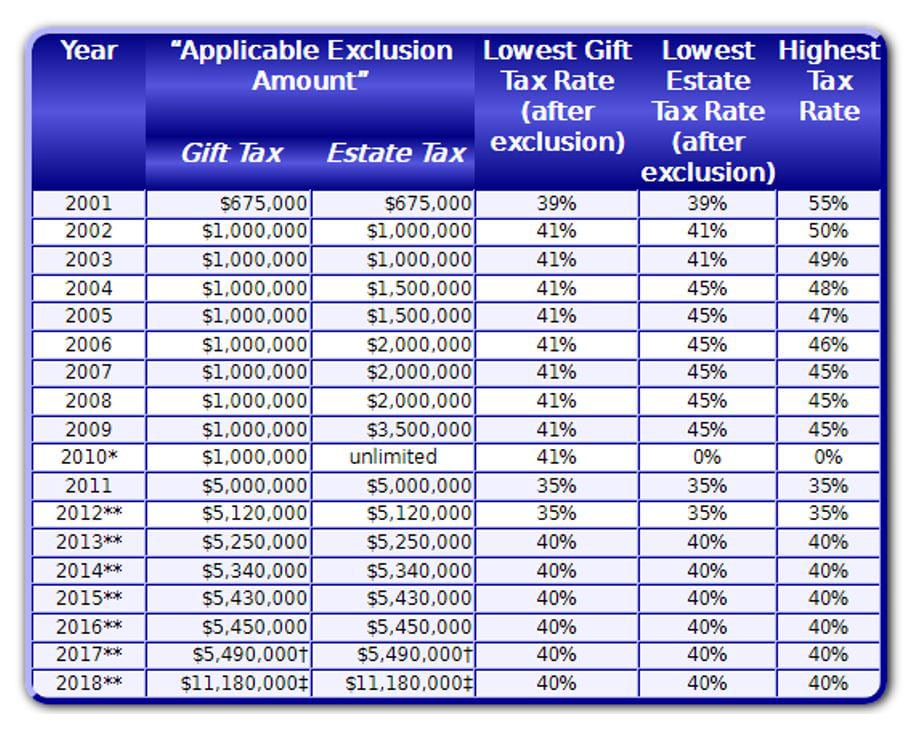

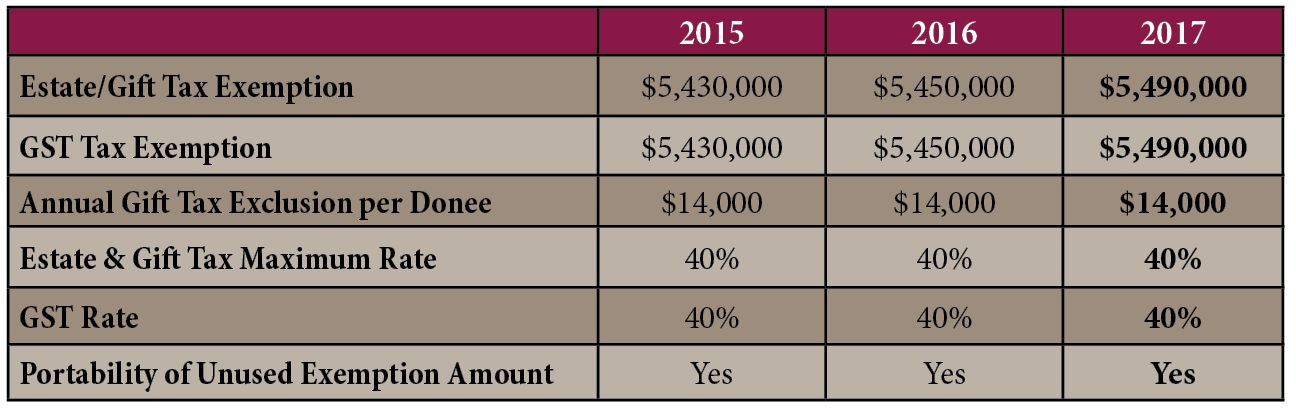

Estate tax return preparers who prepare any return or claim for refund which reflects an understatement of tax liability due to an unreasonable position are subject to a penalty equal to the greater of 1000 or 50 of the income earned or to be earned for the preparation of each such return. Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the. This election must be made on a timely filed Form 706 US Estate Tax Return of.

Connect with our CPAs or other tax experts who can help you navigate your tax situation. This is a bizarre result leaving practitioners and clients troubled and skeptical. Nearly as important when it comes to estate plans for married couples is the advent of the portability of the estate tax exemption the Deceased Spouses Unused Exemption DSUE.

Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. To make a valid portability election the Internal Revenue Code Code requires an executor to make the election on an estate tax return filed within the. The key component to portability is the filing of an estate tax return for the first spouse to die.

Portability of Deceased Spousal Unused Exclusion DSUE is the ability to elect to transfer the remaining unused exemption also known as federal basic exclusion amount from a deceased spouse and add it to the surviving spouses current lifetime exemption. This is called the deceased spouses unused exemption or DSUE. The estate must file a federal return to elect portability but any QTIP election made therein will be treated as null and void.

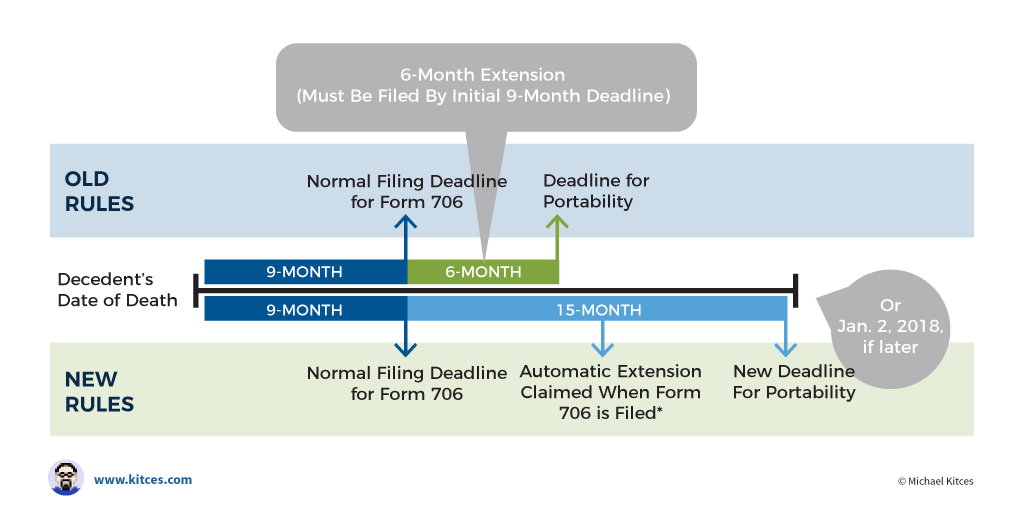

In order to elect portability of the decedents unused exclusion amount deceased spousal unused exclusion DSUE amount for the benefit of the surviving spouse the estates representative must file an estate tax return Form 706 and the return must be filed timely. Estate tax return preparers who prepare a return or claim for refund which reflects. The due date of the estate tax return is nine months after the decedents date of death however the estates representative may request an extension of time to file the return for up to six months.

See 206075-1 and 206081-1 for additional rules relating to the time for filing estate tax returns. Ad Learn how receiving a gift bequest or inheritance affects your income. By simply filing an estate tax return at the death of a spouse even if no estate tax is due the estate tax exemption for the surviving spouse may roughly double.

Again to elect portability the deceased spouses estate has to file an estate tax return and if that isnt otherwise required that introduces some complexity and some cost into that process. Normally an estate tax return is only filed if the decedents estate is valued over the estate tax exemption amount. This portability election increases the total exclusion available to the surviving spouse by the amount of the deceased spouses unused exclusion.

The due date of the estate tax return is nine months after the decedents date of death however the. What Does Portability of the Estate Tax Exemption Mean. Formally this is called the Deceased Spouse Unused Election DSUE.

However if an estate is not otherwise required to file a US estate tax returnbecause the decedents gross estate plus adjusted taxable gifts does not exceed the applicable exclusion amountTreasury regulation section 202010-2a1 provides that the IRS may grant an extension of time to file a return and make a portability election. Importantly under New York law a separate QTIP election is not available. It was 549 million in 2017.

However in order to elect portability an estate tax return must be filed even if the assets are less than the exemption amount. It is transferred to the surviving spouse to reduce the overall estate tax once the second spouse passes away. It essentially allows a surviving spouse to take the remaining estate tax exemption that the deceased spouses estate did not use.

Portability is the right of an executor to transfer or port the unused estate tax exemption from the first spouse to die to the second spouse to die. The IRS acknowledged this issue and. Portability Election on Form 706 The estate of a decedent with a surviving spouse elects portability of the DSUEA by completing and timely filing Form 706.

Portability is the term used to describe a relatively new provision in federal estate tax law that allows a widow or widower to use any unused federal estate tax exemption of his or her deceased spouse to shelter assets from gift tax during the surviving spouses life andor estate tax at the surviving spouses death. Portability occurs when a surviving spouse files an estate tax return for the purpose of calculating and capturing any Estate Tax credit left unused in the estate of the first spouse to die. The Tax Cuts and Jobs Act TCJA effectively doubled the federal estate tax exemption in 2018.

No further action is required to elect portability. An automatic six month extension of time to file the return is available to all estates including those filing solely to elect portability by filing Form 4768 on or before the due date of. Accordingly the due date of an estate tax return required to elect portability is nine months after the decedents date of death or the last day of the period covered by an extension if an extension of time for filing has been obtained.

Will My Executor Be Required To File An Estate Tax Return Vermillion Law Firm Llc Dallas Estate Planning Attorneys

Credit Shelter Trusts And Portability Eagle Claw Capital Management

Portability Of Unused Estate And Gift Tax Exclusion Between Spouses

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

Estate Tax Portability Preserving It For The Benefit Of Your Heirs

The Surviving Spouse Estate Tax Trap When Someone Dies Estate Tax Inheritance Tax

Estate Tax Exemptions 2020 Fafinski Mark Johnson P A

Understanding Qualified Domestic Trusts And Portability

Tax Related Estate Planning Lee Kiefer Park

Federal Estate Tax Portability The Pollock Firm Llc

Exploring The Estate Tax Part 2 Journal Of Accountancy

Special Rule Of Regulations Section 20 2010 2 A 7 Ii Trust Me I M A Lawyer

/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Form 706 Extension For Portability Under Rev Proc 2017 34

The 2017 Estate Tax Exemption The Ashmore Law Firm P C

Estate Tax Introduction Video Taxes Khan Academy

Pin On Taxes And Accounting

Estate Planning Can Secure Your Legacy Jackson Fox Pc Ardmore Ok

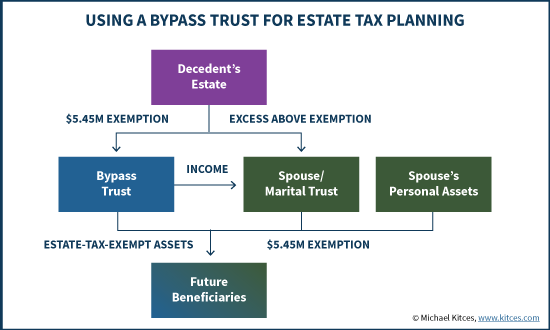

Distributable Net Income Tax Rules For Bypass Trusts